Many people have a limited definition of “distracted driving”: They think it only means texting behind the wheel.

There’s good reason for that, because texting requires visual, manual and cognitive attention – the same attention required for safe driving. But although texting is perhaps the most dangerous distraction, there are many others that can impact how you drive, whether you realize it or not. And they can be just as deadly.

How deadly? According to the CDC, in 2019 more than 420,000 people were injured in crashes caused by distracted drivers – with more than 3,100 killed.

There are three main categories of distraction when it comes to driving:

Visual: Taking your eyes off the road

Manual: taking your hands off the wheel

Cognitive: taking your mind off driving

Here are just a few of the things that can distract drivers on the road:

Talking on the phone, even with a hands-free device.

Eating or drinking.

Talking to passengers.

Grooming (yes, there really are people who apply makeup or shave on their way to work).

Reading, including maps.

Adjusting the stereo.

Younger drivers are the most distracted of all – according to the government’s distraction.gov website, people in their 20s make up 38% of drivers who were using cell phones before a fatal crash, and 10% of teen drivers involved in fatal crashes were distracted, too.

With distractions more prevalent than ever – more than 150 billion text messages are sent in the U.S. every month, for example – how can you, and those you love, be safer behind the wheel? Here are a few tips:

Don’t use the phone: This includes texting as well as talking, unless it’s an emergency. Even hands-free conversations can take your attention off the road.

Eat before you leave, or after you get there: Scarfing down that burger with one hand on the wheel means your focus is divided – and you probably don’t have as much control over your car as you should. Bonus benefit: Keeping your meals and your driving separate means you’re much less likely to get ketchup on your pants.

Know where you’re going: Nobody likes to be lost. But messing around with your car’s GPS (or the maps app on your smartphone) while you’re moving can lead to something you’ll hate even more – an accident.

Talk to your family about safe driving: Having a conversation with your spouse as they’re driving home? That’s a perfect opportunity to say, “I’ll let you focus on the road; we can talk when you get here.” And if you have young drivers in the household, be sure to have a conversation about their phones and other potential issues, such as their passengers – a key distraction for teens.

Watch for other distracted drivers: Just because you aren’t distracted doesn’t mean that other drivers are focused on safe driving. Stay in control and be vigilant – you’ll be ready to react when someone else makes the wrong move.

Distracted driving isn’t just “one of those things” that happens, like a tire blowout or mechanical failure that isn’t anyone’s fault. It’s 100% preventable – and by committing to avoiding distractions while you drive, you’ll help make the road safer for everyone.

You keep your car filled up with gas so you don’t get stranded on the side of the road. And, your phone charged so your loved ones can reach you. But, what kind of safety measures do you have in place for more extreme scenarios?

What if you lost everything you owned in a fire at your house or your apartment? What if your car were stolen? These situations are scary, but your insurance can help you through them, and much more, so long as you have the right coverage in place.

So, what’s right for you? Whether you’re starting out on your own or starting a family, these tips can help you begin to understand the level of insurance you may need.

Consider What You Own – And What It’s All Worth Could you imagine having to replace all of your personal belongings at once? What about having to do so from memory and on your own dime? It would be both a difficult and a costly task. So, make an inventory of your belongings and their value to minimize the former – the free Safeco Home Inventory appcan help. And, be sure you have enough insurance coverage, whether you rent or own a home, to minimize the latter. It’s known as “personal property coverage,” and you want enough of it to replace all of your belongings if it were to come to that.

Take Your Lifestyle Into Account Drive an expensive car? Repairs are likely costly, so be sure to carry comprehensive and collision coverage. Consider any customizations in the car and whether you want original manufactured parts in repairs are needed or if you’re okay with aftermarket. We’re happy to go over your auto coverage options to ensure you have the kind of protection you expect.

Own a home with a lot of custom features? Be sure your homeowners policy takes them into account. The amount of insurance you have on your home should directly reflect the unique features of your home. Your agent should complete a detailed Replacement Cost Estimator to determine the insurance limits needed.

The way you live can help you save, too. For example, if you take public transportation to and from work even though you own a car, you may pay less for your insurance.

Talk to Your Independent Agent for Ease, Choice and Advice As an independent agency, Integrity First Insurance offers a choice of carriers and options, plus personalized advice to help make sense of it all. And, we make it easy by doing the research and the work for you.

Most people would say their car is one of the most valuable assets they own — if not the most valuable. Despite that, however, some people make it downright easy for thieves to drive off in their pride and joy.

At Integrity First Insurance, we don’t want you walking out your door to an empty driveway or leaving a store only to find some broken glass left behind in your parking space. So take care to avoid these five mistakes.

Leave your car running … and unattended. We know it can be chilly in the mornings, and who wants to wait in a cold car while it warms up? Well, a thief certainly won’t mind the chill — as he’s driving away in your car while you’re finishing that cup of coffee in your kitchen. If your car is running, you should be in it. Period. Even if you’re just running over to the ATM to get some cash or dropping off some mail.

Keep a spare set of keys inside the car. Law enforcement agencies say this is a great way to turn a car prowler into a car thief. They’re already breaking into your car to get a phone, or a laptop, etc. What do you think they’re going to do when they find a set of keys? They’re not going to drop them off on your porch with a nice note, that’s for sure.

Put valuables in plain sight. Seems simple, but we’ve all made this mistake. You’ll just be in the store for a second, after all, so who cares if you leave your smartphone on the front seat? Or items from your other errands in the back seat? Be smart — if you have to leave items in your car, put them in the trunk, or at least hide them as best you can. And do it before you get to your next destination.

Leave your car unsecured. The best thieves can work wonders with a window that’s left open even just a crack. And even the worst thieves can steal a car that’s been left unlocked, with no alarm set.

Assume nobody would want to steal your car. Think your car is too old or too undesirable for a thief to bother? Scrap metal is worth money, so never assume that your car is safe — even if you think it’s just a “junker.”

Keeping thieves away helps to keep everyone’s insurance costs down, so avoiding these mistakes not only will save you hassle, it will save you money as well. So stay safe, not only on the roads, but in the parking lots as well!

When teens begin to drive, according to the National Highway Traffic Safety Administration (NHTSA) and the National Safety Council, the sobering statistics start to pile up:

Car crashes are the leading cause of death for U.S. teens ages 14 through 18.

A teen’s crash risk is three times that of more experienced drivers.

Being in a car with three or more teen passengers quadruples a teen driver’s crash risk.

More than half of teens killed in crashes were not wearing a seat belt.

You can help your young driver make better decisions behind the wheel, however. Start by setting a good example yourself. And set time aside to have a serious discussion about the following issues, all of which have a large impact on the safety of teen drivers:

Speed: According to the Governors Highway Safety Association, speeding continues to grow as a factor in fatal crashes involving teen drivers. Thirty-three percent of such accidents in 2011 involved excessive speed. While a lot of emphasis is rightfully placed on the risks of driving under the influence or while distracted, the danger of speeding is just as important.

Alcohol: If drivers are under 21, driving with any amount of alcohol in their system is illegal. It’s as simple as that. And not only does the risk of a serious crash increase once alcohol is involved, jail time is a possibility as well.

Seat belts: Teens don’t use their seat belts as frequently as adults, so it’s important to set a good example and always have yours on. Seat belts are the simplest way to protect themselves in a crash, so let teens know that buckling up is mandatory.

Phones: Distracted driving is dangerous driving, especially for an inexperienced teen. That means no calls or texting when behind the wheel — no exceptions. Again, it pays to set a good example when you’re driving with your teen in the car.

Passengers: The risk of a fatal crash goes up as the number of passengers in a teen driver’s car increases, according to the NHTSA. Depending on your state’s licensing laws for young drivers, limiting your teen to one passenger is a good guideline. (And some states don’t allow teens to have any passengers for a time.)

Of course, any driver needs to have a good grasp on the laws and rules of the road, and, because teens don’t have much experience, it’s important to have regular conversations about safe driving. How teens drive doesn’t just depend on them. It depends on you, too!

The days are short. The air is cold. And, roads are often slick with rain, snow or ice.

It’s winter driving season in Colorado. And, while most people know what to do to try to avoid an accident, many don’t know what to do after one. It’s vital knowledge to have, because the aftermath of a crash can be just as dangerous as the crash itself — especially when it’s cold and snowy.

Here are five things to do (or not do) if you’re in an accident this winter to help keep yourself and others safe:

Make sure everyone’s OK — then get off the road if you can. The safety of everyone involved in a crash is the first concern, of course. So, check on the occupants of each vehicle and call for emergency assistance if it’s needed. Then, if the vehicles are drivable, get them off the road as soon – and as carefully – as possible.

Stay in your car if you can’t safely move away. If you can’t get your car off the road, but you can get off the road, wait until there’s no traffic around and then move well out of the way. Otherwise, stay in the car so you’re protected from other vehicles.

Stay visible — and warm. Turn on your hazard lights and put up road flares so other vehicles know something is wrong. And, grab your vehicle emergency kit (you have one, right?) for blankets and extra clothing. If you’ve run off the road and you’re still in your car, make sure nothing is blocking your exhaust pipe. Otherwise carbon monoxide may build up.

If you’re stranded, stay put. Running off the road in a remote area is scary, but resist the urge to try to walk for help. You risk getting lost, especially during a storm, if you set off on foot.

See a crash? Don’t always stop to help. Being a Good Samaritan could cause more problems than it solves. So, if those involved aren’t in immediate danger, call 911 and let the professionals help with medical aid and traffic control.

It’s not always easy, but keeping a cool head after an accident will do more than help everyone get through a stressful situation — it will help keep everyone safer, too.

And, remember, if something does happen on the road this winter, Integrity First is here to help with your auto accident claim. If you’re unsure whether you’re carrying the right coverage, call now before it’s too late!

Safe driving saves lives. If you’re traveling this holiday season, follow these tips to protect yourself and others on the road with you.

Traveling during the holidays brings us closer to family and loved ones, but sometimes, traveling also puts us in harm’s way. According to the National Safety Council, 406 people died in traffic accidents during the Thanksgiving weekend in 2019. This number is not atypical for the holiday season: NSC consistently estimates that between 400 and 500 people will die over the 4-day period we celebrate Thanksgiving.

Take steps to protect yourself and your loved ones. The following tips can help you avoid accidents that can lead to injuries and even fatalities.

Wear a Seat Belt

Seat belts save lives. According to the United States Department of Transportation, seat belts saved nearly 15,000 people who survived car accidents in 2017. Whether you’re going to see a relative in your town or traveling hundreds of miles from home, wear a seat belt. Be sure the other people in your vehicle buckle up as well.

Pay Attention to the Weather

Thanksgiving weather can vary, from snowy to icy to beautiful and sunny. Pay attention to the weather at your point of departure, your destination, and the route in between. Watch for low temperatures, chances of precipitation, and more.

Know Your Route

How will you be arriving at your destination? If you’re using a GPS device or GPS on your smartphone, plug in the route before you start driving.

Avoid Drowsy Driving

Drowsy driving caused over 600 traffic deaths in 2020. Driving drowsy can reduce your reaction time and cause you to fall asleep behind the wheel. To avoid drowsy driving:

Drive with a partner and take turns driving

Get out to walk around periodically

Avoid driving at times when you would usually be sleeping

Drink coffee or another caffeinated beverage

If you’re feeling tired, roll down your window to increase your alertness

Listen to music or talk to people in the car with you to increase your alertness

Divide long journeys into segments and know when to stop for the night

Put Children in Appropriate Seat Restraints

Children are required to ride in seat restraints. The youngest children must ride in rear-facing car seats until they graduate to front-facing car seats and, finally, booster seats. Pay attention to the weight requirements for each type of car seat, and know the seat restraint laws in your state.

Watch Your Speed

Of course, you should follow the posted speed limits along your route, but sometimes driving the speed limit is too fast for your journey. The speed limit may be dangerously fast if the road is icy, wet, snowy, or in poor condition. Use common sense when selecting your speed. Don’t prioritize a quick journey over the safety of you and your passengers.

Don’t Drive Distracted

Over 3,000 people die in distracted driving-related accidents every year. Pull over if you must take a call, send, or read a text message while driving. If someone is in the car, let them take the call, change the radio station, read the text message aloud, and adjust your GPS device. Never read or send a text message while driving.

Drive Sober

In 2019, nearly 1/3 of traffic fatalities involved alcohol. Alcohol-related traffic deaths are entirely preventable. It’s common for people to have a drink or two when at a relative’s house for a holiday celebration. Before arriving at your destination, designate a sober driver – or plan to stay the night.

Update Your Auto Insurance Policy

Take steps to protect yourself this holiday season. Call your insurance agent to check (and update) your auto insurance policy.

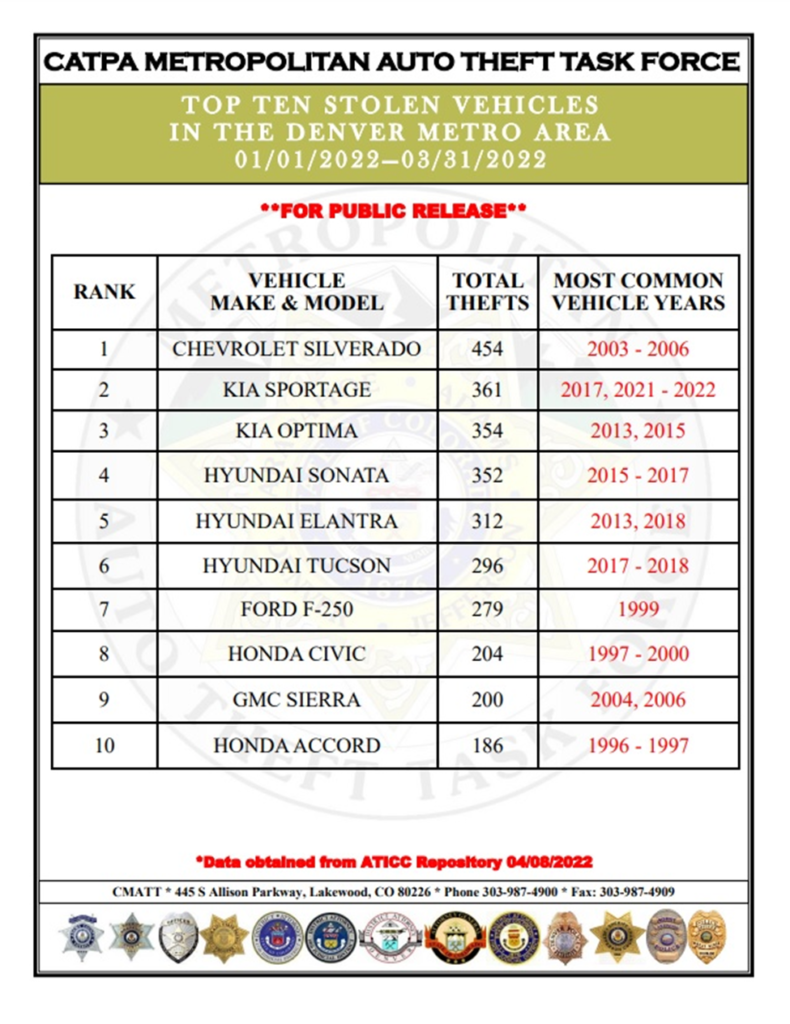

According to data provided by the Colorado Metropolitan Auto Theft Task Force (CMATT), car thefts in Colorado have increased by 173% in the past 3 years. That makes Colorado the No. 1 state in the nation for car thefts per capita, as reported by the National Insurance Crime Bureau.

What is causing the number of car thefts to soar in Colorado?

One contributing factor is the growing homeless population in Denver. Many car thieves that are repeat offenders are part of the homeless population and use the stolen cars as shelters. Though most stolen cars are eventually recovered, the thief is often long gone and never found.

The relatively lax laws against car theft also play a significant part in the increasing rate of car theft. Even when thieves are caught, they tend to get out within days and see little to no punishment. The lack of real repercussions for car thieves makes it a low risk/high reward crime, leading to many repeat offenders.

Which vehicles are most at-risk of being stolen?

The Colorado Auto Theft Prevention Authority (CATPA) released a list of the 10 most-stolen vehicles in the Denver metro area from January-March 2022:

What can you do to prevent your car from being stolen?

No “Puffing.” Don’t leave your car running when you’re not in it.

Lock your car and roll up your windows. Leaving it unlocked, the windows down (even just a crack), or leaving a spare key in or on the car makes a thief’s job much easier.

Park in a garage if you can. Significantly fewer cars are stolen from garages than from driveway, streets, or parking lots.

Park in well-lit areas. Both in public and at home. If you park in your driveway or on the street at your house, consider adding a bright light to reduce shadows where a thief could hide.

Don’t leave valuables in your car. Many cars are targeted because the thief sees money, a computer, a camera, a purse, or some other valuables inside.

Install an outdoor camera that covers the area where you park your car. Just the presence of a camera can deter a would-be thief, and if your car is stolen it can help identify the culprit.

A catalytic converter is part of a vehicle’s exhaust system that helps turn toxic pollutants into cleaner emissions.

Why are they being targeted?

They are made of precious metals, commonly platinum, palladium and rhodium, all of which can be sold for high prices. A single catalytic converter can be sold for as high as $1,500.

Since they are easy to steal, many can be stolen in a short period of time. Since they are easy to steal and worth a pretty penny, they are a prime target for thieves to make money quickly.

Where are vehicles most at-risk?

Cars that are parked in public spaces are the most likely to have their catalytic converter stolen. Places where cars are likely to be parked for a longer period of time, like a Park-N-Ride or airport parking lot, are the most commonly targeted.

Which vehicles are targeted the most?

According to Denver7, Hondas and Toyotas are the most targeted vehicles in the Denver area.

What can you do to prevent your catalytic converter from being stolen?

The police don’t recommend confronting someone if you see them trying to steal your catalytic converter. There’s a pattern of thieves pulling weapons when confronted. It’s safer to call the police and report the theft in-progress while keeping a safe distance.

Some steps you can take to prevent theft:

Park in a garage or well lit area

Have the bolts holding the catalytic converter welded in place

Put a cage around it

Get your VIN engraved on the catalytic converter, which may deter theft or increase the chances of finding your missing part

Contreras, Ó., & Miller, B. (2022, April 4). Catalytic converter thefts: What cars are being targeted, where it’s happening, & how to protect yourself. Denver 7 Colorado News (KMGH). Retrieved August 30, 2022, from https://www.thedenverchannel.com/news/360/catalytic-converter-thefts-what-cars-are-being-targeted-where-its-happening-how-to-protect-yourself

Auto theft prevention tips- CATPA – all about puffer cars. CATPA. (2022, July 6). Retrieved August 30, 2022, from https://lockdownyourcar.org/prevention/

Fields, M. (2022, July 18). Fields: Aurora offering a model solution to Colorado car theft tsunami. Sentinel Colorado. Retrieved August 30, 2022, from https://sentinelcolorado.com/opinion/fields-aurora-offering-a-model-solution-to-colorado-car-theft-tsunami/

Friday. (2022, July 1). Year-to-date Colorado car thefts outpacing 2021. Colorado State Patrol. Retrieved August 30, 2022, from https://csp.colorado.gov/press-release/year-to-date-colorado-car-thefts-outpacing-2021

Kovaleski, J. (2022, June 21). Here are the areas where your car is most likely to get stolen in the Denver Metro Area. Denver 7 Colorado News (KMGH). Retrieved August 30, 2022, from https://www.thedenverchannel.com/news/investigations/here-are-the-areas-where-your-car-is-most-likely-to-get-stolen-in-the-denver-metro-area

Nieto, G. (2022, April 14). Top 10 most-stolen vehicles in the Denver Metro. FOX31 Denver. Retrieved August 30, 2022, from https://kdvr.com/news/local/top-10-most-stolen-vehicles-denver-metro/

Pender, C. (2022, August 9). Why do people steal catalytic converters? KRON4. Retrieved August 30, 2022, from https://www.kron4.com/news/why-do-people-steal-catalytic-converters/#:~:text=The%20three%20precious%20metals%20that,%2C%20according%20to%20cars.com.

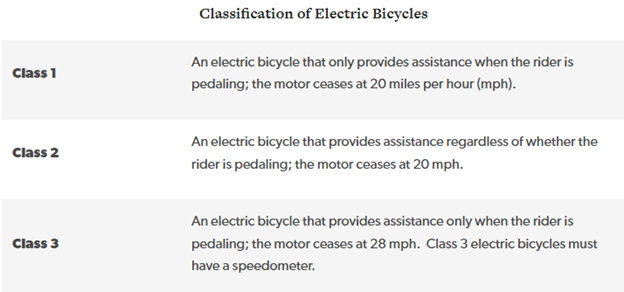

According to Colorado Parks & Wildlife, an E-bike has 2 or 3 wheels, fully operable pedals, and an electric motor that doesn’t exceed 750 watts of power.

There are 3 classes of E-bikes:

Important Colorado E-bike laws:

Electronic bicycles are not required to be registered

There are no license requirements for E-bikes

Generally speaking, Class 1 and 2 E-bikes are allowed to operate on the same paths as conventional bikes, thought local jurisdictions can prohibit operation on specific paths

Class 3 E-bikes are only allowed on streets and bike lanes, unless specifically permitted by local jurisdictions

There are different rules pertaining to State Park or Wildlife Areas

E-bikes must ride in the right-hand lane when traveling a less than the normal speed of traffic on a roadway

Riders must signal intent to turn or stop and yield the right of way to pedestrians

One hand must be kept on the handlebars at all times

Class 3 E-bikes have the following age and helmet restrictions:

Operators must be 16 or older (passengers can be under 16)

Operators and passengers under 18 must wear a helmet

Does an E-bike have to be insured?

The short answer is no. There aren’t any legal requirements to insure an E-bike. That being said, if you have a loan on an E-bike, your lender will likely require you to carry insurance on it.

Even though you’re not required to have insurance on an E-bike, it’s important to at least have liability coverage. You can go faster on an E-bike than you might otherwise travel on a conventional bike, which makes the risk of crashing a little higher. If you hit a person, fence, house, mailbox, or something else, you could be responsible for the damages. Liability insurance will help you pay for those damages if a situation like that arises.

If you’ve paid a pretty penny for your E-bike, it probably makes sense to get adequate insurance for it. That way if it gets stolen, damaged in a fire, you’re in an accident, or something else happens, you’re not left empty handed.

How to insure an E-bike:

Many homeowners policies will afford some amount of coverage for an E-bike. Some policies may only extend liability, whereas others have a special limit of physical damage coverage included and some may not extend any coverage at all. Each insurance carrier has their own guidelines, so be sure to check what coverage you have on your policy.

Keep in mind that most home policies have a deductible of $1,000 or higher, so if you’re counting on your home policy to cover any damages to your bike you’ll need to cover your deductible before your policy pays out. Depending on the value of your E-bike and your home insurance deductible, it might not make sense to insure it on your home policy.

Many E-bikes cost several thousand dollars, so a total loss might exceed your deductible. But if a $1,200 E-bike was stolen, that’s not a claim I’d recommend filing on a home policy. You’d only get $200 from that claim example, which isn’t worth having a claim against your home insurance since it would likely cause your premium to increase for up to 5 years.

If you don’t have a home policy or if your policy doesn’t provide the coverage you’re looking for, you can generally insure and E-bike on a motorcycle policy. One benefit of that is that you can choose a lower deductible, like $500 or even lower.

Another plus is that you can file a claim without it impacting your home insurance. A claim for a stolen E-bike wouldn’t cause your motorcycle premium to increase like it would if you filed a claim on your home policy.

Insuring an E-bike on a motorcycle policy would also give you the option of Medical Payments and Uninsured Motorist coverage, both of which can be extremely valuable. Medical Payments coverage can help pay for your injuries, regardless of whether you’re at fault for a loss. The limit is usually $5,000 per person, but limits can vary.

Uninsured Motorist coverage will help cover your costs if you’re not at-fault for in an accident and the other person doesn’t have enough coverage. You can get Uninsured Motorist coverage up to the bodily injury liability limits on your motorcycle policy.

Colorado Parks & Wildlife. Colorado Parks and Wildlife. (n.d.). Retrieved June 27, 2022, from https://cpw.state.co.us/thingstodo/Pages/E-Bike-Rules.aspx

Electric Bicycles. Electric Bicycles | Colorado General Assembly. (n.d.). Retrieved June 27, 2022, from https://leg.colorado.gov/content/electric-bicycles

In the insurance industry, a “catastrophe” is a disaster that is unusually severe and meets or exceeds a loss threshold. As of December, 2021, the current dollar threshold to declare an event a catastrophe is $25 Million, according to Insurance Information Institute. Some examples of catastrophic events include tornadoes, hailstorms, high wind, flooding, hurricanes and wildfires.

Colorado does see some flooding and tornadoes, but the largest losses come from wildfires and hailstorms. Colorado has the 3rd highest wildfire risk in the US and had the 2nd most hail claims filed between 2018-2020.

Wildfire

Insurance Information Institute reported that as of October, 2021, Colorado has 373,900 properties with “high to extreme wildfire risk.” That makes up 17% of the properties in the state. With so many properties at risk of being damaged or destroyed by wildfire, insurance companies have to plan accordingly.

Colorado’s highest catastrophic payouts since 2017:

May 8, 2017 Denver Metro Hailstorm: $2.3 Billion

2018 Front Range & CO Springs Top 3 Hailstorms: $276.4 Million, $169 Million, $172.8 Million

2020 East Troublesome Fire: $543 Million

2021 Marshall Fire: Over 1000 structures destroyed and estimated $1 Billion in damages

The high wildfire risk in Colorado means higher rates across the state. But insurance companies charge more for insurance on homes that have the highest risk. They do this by assigning each property a Protection Class (PC) or Brushfire Score, which determines the risk of fire and the responding fire department’s ease of access and resources. The higher the PC or Brushfire Score, the higher the premium charged to insure that property.

Colorado has the 3rd highest wildfire risk in the US and had the 2nd most hail claims filed between 2018-2020.

Hail

Hail has been a problem in Colorado for as long as I can remember, but the number and severity of claims have increased significantly over the past decade. Part of that is due to the increasing population in the state. The more homes that are built on the Front Range, the more targets there are for hail to hit.

Between January 1, 2017 and December 31, 2019, Denver and Colorado Springs were in the top 5 cities for hail losses, with Denver at #2 and Colorado Springs at #3, according to an Insurance Journal article. Insurance companies in Colorado pay out hundreds of millions, if not over a billion dollars for hail damage every single year. Most companies have higher deductibles for wind and hail losses to help mitigate the risk. They also have to charge an adequate amount for both auto and home insurance.

2. Traffic Accidents

There are three major factors causing the number and severity of traffic accidents to rise in Colorado: Booming Population, Impaired Driving, and Distracted Driving.

Population Growth

It’s no secret that the population in Colorado is increasing at a rapid rate. According to U.S. News, the 2020 Census showed that Colorado was 6th fastest-growing state from 2010-2020, with a 14.8% growth. Unfortunately, traffic infrastructure has not kept pace with the population growth, leaving many roads on the front range gridlocked more frequently than not. More cars on the road directly correlates with accident frequency.

Distracted Driving

In addition to the heavier traffic, dangerous driving activities are becoming more common. Nearly everyone has a smart phone, and most people don’t put their phone on “Do Not Disturb” when they get behind the wheel. Distracted driving can include anything that takes focus away from the road, including texting, talking on the phone, eating, reading, and more.

91% of participants reported driving distracted in the past seven days. 54% admitted to reading a message on their phones. Nearly 50% talked on a cell phone while driving. 41% sent a message while driving.

CDOT also reported that in 2020, 10,166 crashes in Colorado involved distracted drivers. Those accidents caused 1,476 injuries and 68 deaths.

Impaired Driving

Impaired driving is also contributing to more severe and frequent accidents. The total number of fatal crashes has increased by 37% from 2011 to 2021. Fatalities involving drivers that tested positive for drugs increased by 39.3% from 2015 to 2019. Drivers with a BAC over the legal limit were involved in 8.6% more fatal accidents during that same time.

From 2020 to 2021, the number of DUIs involving marijuana went up by 48%. While not all DUI incidents end in an accident, the increase in risky driving behavior certainly impacts the frequency of crashes.

With impaired and distracted driving causing more crashes, injuries and fatalities, insurance companies are paying out more for auto claims in Colorado. Higher medical costs are also impacting the higher payouts for auto accidents. Berkley Accident and Health reported that treatment costs increased by 6% in 2020 and another 7% in 2021.

Unfortunately when accident frequency and severity increases, we all pay the price. The more insurance companies pay out in claims, the more rate increases they are forced to take in order to remain solvent in the state.

3. Supply Shortages

There have been worldwide supply shortages since the pandemic started in 2020, which have led to inflated prices across most industries. Since the materials for home construction and auto parts are more expensive, insurance payouts are also inflated.

Auto Part Shortages

According to the Consumer Price Index, the cost of auto parts have increased by 14.2% from March 2021-March 2022. Insurance companies generally consider a vehicle a total loss if it will cost more than 70% of the vehicles value to repair the damage. That means more cars are being totaled because of the inflated repair costs.

Both new and used cars are also much more expensive than they were a few years ago. Supply chain disruptions have made it harder for manufacturers to produce enough new vehicles. There were 7.7 Million fewer vehicles produced in 2021, largely due to the microchip shortages. The shortfall of new vehicles directly impacts the price of used vehicles.

As the values of used vehicles increase, the payouts for total losses get higher. With insurance companies paying out more, the cost of insurance also goes up.

Building Material Shortages

On top of the rising costs impacting auto insurance, the costs of building materials have also soared because of supply chain shortages. Lumber prices jumped 42% in the first year of the pandemic, and steel mill products rose 81% in the first three quarters of 2021. Throughout 2021, the price of materials for new construction increased by over 18%.

The inflated cost of materials alone has led to much higher prices for rebuilding homes that have been damaged. Just like with auto insurance, higher home claim payouts leads to home premium increases.

On home policies, insurance companies are increasing rates to keep up with the amount they are paying out for claims but premiums are also rising due to higher coverage amounts. Since it costs more to rebuild a home, the amount of coverage you have on your home policy is likely also increasing.

There’s a good chance that if your policy was written more than a year ago, you don’t have enough coverage to rebuild your whole home.

You may have been able to rebuild your home for $150/square foot 4 or 5 years ago, but now it might cost closer to $275/square foot. As a result, your dwelling coverage (Coverage A) needs to increase to ensure your home is properly insured.

Many homeowners found out they were underinsured after the Marshall Fire, which is largely due to the rapid inflation seen in the past several years. If you haven’t review your home coverage with a licensed agent recently, I highly recommend you do. There’s a good chance that if your policy was written more than a year ago, you don’t have enough coverage to rebuild your whole home.

You can walk into almost any business and see a “Help Wanted” sign on the door. It’s no secret that there are labor shortages across most industries. The shortage of workers has directly impacted the supply shortages, but even when the supplies are available many industries don’t have enough people to actually do the work.

Auto Technician Shortages

There’s currently a deficit of trained auto technicians to work on repairing damaged vehicles. To keep up with demand, there needs to be 3 times as many qualified technicians. The shortfall of auto technicians is causing higher auto repair costs and longer repair times.

When it takes longer to repair a vehicle, the insurance companies end up paying for a rental car for longer which also increases the claim payout amount.

Skilled Construction Labor Shortages

When it comes to home construction, there’s a shortfall of at least 200,000 skilled trade workers. That has led to more expensive bids for both home repairs and new construction. Not only are skilled workers charging more for their labor, but the amount insurance companies are paying for Additional Living Expenses is much higher.

Most home policies come with coverage for Additional Living Expenses, so if you can’t live in your home due to a covered loss they will pay for the additional expenses you incur as a result. That includes a hotel or long-term rental, restaurant expenses if you don’t have a kitchen to cook in, dry cleaning bills if you don’t have access to a washer and dryer, and more. If takes 6 months longer to rebuilt your home after a loss, the insurance company is paying those expenses for longer.

At the end of the day, the amount insurance companies pay out for claims directly impacts the amount they charge for insurance. All of the reasons listed above are causing insurance companies to pay out more than they have in the past. As a result, the cost of auto and home insurance are increasing accordingly.

Boyd, S. (2021, January 29). Marijuana Dui Arrests Up 48% In Last Year Across Colorado. CBS Denver. Retrieved April 13, 2022, from https://denver.cbslocal.com/2021/01/29/marijuana-dui-colorado-arrests-alcohol/

Catastrophe Facts & Statistics. RMIIA. (n.d.). Retrieved April 13, 2022, from http://www.rmiia.org/catastrophes_and_statistics/catastrophes.asp#:~:text=The%20most%20destructive%20wildfire%20in,and%20auto%20insurance%20claims%20filed

Davis Jr., E. (2021, April 28). 2020 census shows America’s fastest-growing states | best … U.S. News & World Report. Retrieved April 13, 2022, from https://www.usnews.com/news/best-states/slideshows/these-are-the-10-fastest-growing-states-in-america

Distracted driving. Colorado Department of Transportation. (2022, April 4). Retrieved April 13, 2022, from https://www.codot.gov/safety/distracteddriving

Facts + Statistics: Wildfires. Insurance Information Institute. (n.d.). Retrieved April 13, 2022, from https://www.iii.org/fact-statistic/facts-statistics-wildfires

Spotlight on: Catastrophes – Insurance Issues. Insurance Information Institute. (2021, December 13). Retrieved April 13, 2022, from https://www.iii.org/article/spotlight-on-catastrophes-insurance-issues

Top states, cities for insurance claims for hail damage. Insurance Journal. (2020, April 28). Retrieved April 13, 2022, from https://www.insurancejournal.com/news/national/2020/04/28/566579.htm

U.S. Bureau of Labor Statistics. (2022, April 12). Table 7. consumer price index for all urban consumers (CPI-U): U.S. city average, by expenditure category, 12-month analysis table – 2022 M03 results. U.S. Bureau of Labor Statistics. Retrieved April 13, 2022, from https://www.bls.gov/news.release/cpi.t07.htm

Unni, C. (2021, November 29). The Pandemic’s Lasting Effects: Medical Costs Projected to Rise 6.5% in 2022. Berkley Accident and Health. Retrieved April 13, 2022, from https://www.berkleyah.com/the-pandemics-lasting-effects-medical-costs-projected-to-rise-6-5-in-2022/

Across the insurance industry, rates are expected to increase even more this year than they have in recent years. While annual increases are becoming the norm, the jump may be more drastic in 2022.

There are many factors that are driving insurance costs up. Claim payouts are higher than ever, and natural disasters and car accidents are becoming more frequent. Combine that with supply chain issues and labor shortages, and you have the unprecedented market we’re currently in.

Homeowners

Building material costs are at an all-time high

With global supply chain issues and labor shortages, prices for many products have soared over the past few years. Building materials are no exception.

During the first year of the pandemic, the cost of lumber jumped up by 42%. The prices have fluctuated since, but aren’t back to the pre-pandemic prices. In the first three quarters of 2021, steel mill products rose in cost by 81%.

There’s also currently a shortage of at least 200,000 skilled trade workers. 60% of surveyed builders are reporting labor shortages and the vast majority of them don’t expect that problem to go away in the next 6 months.

Price increases from December 2020 – December 2021:

Floor Coverings 3.9% Window Coverings 8% Major Appliances 6% Overall Construction Supplies 18.4%

All of these factors have led to more expensive construction projects for both home repairs and new construction.

Home claims are rising in both severity and frequency

Catastrophic home claims are no longer few and far between, they seem to be happening every other week somewhere in the country.

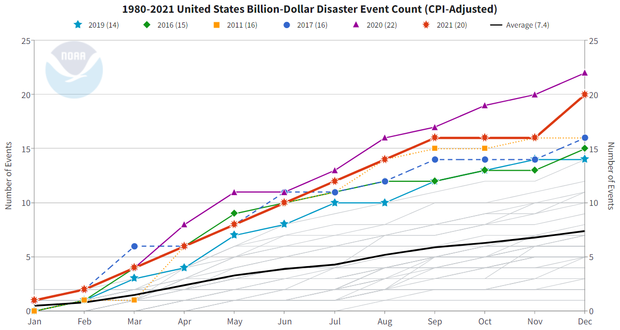

In 2021, there were 20 natural disasters with losses exceeding $1Billion in the US alone. From 1980-2021 the annual average is 7.4 events, but the annual average in the past 5 years is 17.2 events.

Many scientists and experts attribute the increased frequency of disastrous events to climate change. As our weather and climate changes, severe weather events are becoming more common and severe.

Between the increased frequency and severity of home claims and the higher cost of building materials, home insurance prices will continue to increase. The chances that you’ll need to file a claim on your home are higher, and it will cost even more to repair or rebuild your home than it has previously.

Auto

Supply chain disruptions are causing costly shortages

Supply chain issues are impacting many different industries, including auto production. 7.7 Million fewer vehicles were produced in 2021 due to supply chain complications.

One of the most impactful shortages has been microchips that are used in vehicles. With most vehicles containing higher levels of technology than ever before, it’s been difficult for manufacturers to keep up with demand.

Because of the microchip shortage, there’s a shortfall of new vehicles on the market, which has driven up the cost of used vehicles.

Price increases from December 2020 – December 2021:

New Vehicles 11.8% Used Vehicles 37.3%

Many rental car companies sold a large portion of their vehicles in order to survive during the pandemic. Once travel increased again over the summer of 2021, they had to restock their fleet of vehicles. With fewer new vehicles on the market due, they turned to used vehicles.

Around the same time, consumers who had extra money from stimulus checks also began shopping for new and used cars. The combination of that and the rental car companies drove the prices of used vehicles up significantly in June. Those prices remained inflated through the end of 2021 and aren’t expected to drop anytime soon.

The cost to repair vehicles keeps rising

In addition to the microchips, there are also supply chain issues impacting wiring harnesses, plastics, and glass used by auto manufacturers. As a result, the cost to repair vehicles is up around 20% and the cost of auto parts is up 6%.

Similar to the skilled labor shortage seen in the construction industry, there’s also a need for 3 times as many trained auto technicians. The delays in obtaining auto parts and the lack of skilled technicians to complete the repairs have made auto repairs take significantly longer.

With cars being stuck in the shop for longer than usual, that takes up even more of the rental car market. People are needing rental cars for longer, and they are harder to find. That drives the cost of rental cars up and exhausts the car insurance coverage limits faster.

Driving has returned to pre-pandemic levels

At the beginning of the pandemic there were fewer drivers on the roads and there were fewer accidents as a result. During that time, many insurance companies decreased premiums and offered credits or refunds.

In 2021, however, we saw a return to pre-pandemic driving levels and a rise in the number and severity of accidents. Insurance companies found themselves with underpriced policies, which is causing them to now increase rates to keep up with the high claim payouts.

If you’d like to discuss your insurance options or get a proposal, give us a call today. We’re here to help!

Semiconductor shortages to cost the auto industry billions. AlixPartners. (2021, September 23). Retrieved January 27, 2022, from https://www.alixpartners.com/media-center/press-releases/press-release-shortages-related-to-semiconductors-to-cost-the-auto-industry-210-billion-in-revenues-this-year-says-new-alixpartners-forecast/

Smith, A. B. (2022, January 24). 2021 U.S. billion-dollar weather and climate disasters in historical context. 2021 U.S. billion-dollar weather and climate disasters in historical context | NOAA Climate.gov. Retrieved January 27, 2022, from https://www.climate.gov/news-features/blogs/beyond-data/2021-us-billion-dollar-weather-and-climate-disasters-historical

U.S. Bureau of Labor Statistics. (2022, January 12). Table 2. consumer price index for all urban consumers (CPI-U): U. S. city average, by detailed expenditure Category – 2021 M12 results. U.S. Bureau of Labor Statistics. Retrieved January 27, 2022, from https://www.bls.gov/news.release/cpi.t02.htm